In the case of a startup at the early stage, cash is king, and taxes can be regarded as a problem that can be addressed later, after the company reaches profitability. Nonetheless, the One Big Beautiful Bill Act (OBBBA) has also changed a technical R&D provision to a strong liquidity driver in 2026.

Under the new permanent structure of Section 174A, startups are no longer required to wait to have a profitable year in order to receive a tax credit in recognition of their innovation. Instead, they will be able to transfer their research credits into instant tax payoffs in payroll, retaining up to half a million dollars of cold, hard cash in the business.

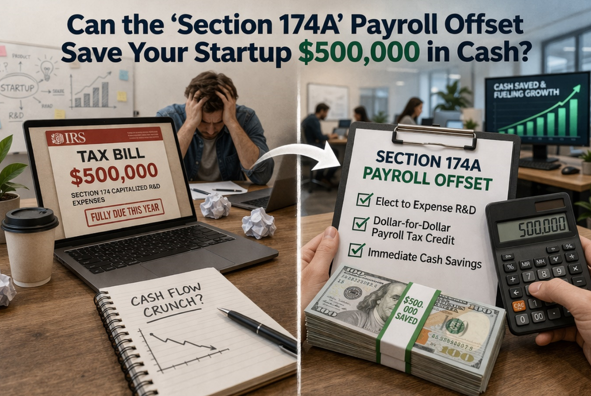

How does Section 174A turn R&D into immediate “Payroll Cash”?

The majority of tax credits are meant to take care of income tax. In the case of a company that did not have a huge amount of net income and had a significant expenditure on R, and the rate was also a startup, such credits usually remain unspent on the balance sheet.

This is modified in Section 174A, where a Qualified Small Business (QSB) has a choice of applying its research credits to the employer portion of the social security taxes. Even in the CDTFA audits, the experts can help the founders.

This election is, in effect, converting in 2026 a paper credit into a cash offset. The start-up pays its payroll taxes through R&D credits to the IRS as opposed to checking every month. This saves the cash runway of the company, and the money can further be put into engineering talents or scaling the product instead of depositing it in federal taxes.

What is the “$500,000 Cap” and who qualifies for it?

The OBBBA cemented the expanded cap on payroll tax offset at the mark of 500000 per annum. A startup should fit within the QSB requirements to receive this “cash-back” system in 2026:

Gross Receipts: The gross receipts must be below 5 million dollars for the current tax year of the company.

Five-Year Rule: The company should not have had any gross receipts during any tax year before the preceding five-year period ending with the present year.

Assuming a high-tech company that is growing fast, and founded in 2022, it would be a good year to be as close to 2026 as possible before they exceed the five-year limit.

Does the “Immediate R&D Expensing” rule accelerate the offset?

Yes. The OBBBA reinstated 100 percent of immediate expensing on domestic R&D expenditures under the umbrella of 174A. In the past, businesses were required to know these expenses over a period of five years, hence reducing the process of generating tax credits. Even in the sales tax audit, the correct cost estimation of R&D can help the founders to get a deduction.

The OBBBA creates a huge credit pool immediately because it enables the write-off of 100% of engineer salaries, software subscriptions, and supplies used in the laboratory in the year they are incurred.

This makes sure that a small engineering department is able to build up enough credits to reach the payroll offset cap of 500,000 as soon as possible, making the most money in cash stay within the operating account of that company.

See also: Reliable Residential Electricians That Make Life Easier

How do you claim the offset on Form 941?

Cash savings as realized are to be reported on 941, the Quarterly Federal Tax Return of the Employer. You then use the credit in your quarterly reports to the payroll after you file Form 6765 with your annual filing of income tax, and have elected the payroll offset.

The IRS has simplified the “Real-Time Verification” of these credits in 2026. After the election is made, the startup just decreases its quarterly tax deposit by that credit.

In case the credit is more than the Social Security tax during a particular quarter, the OBBBA will carry forward the excess to the following quarter so that not even a single dollar of the $500, 000 benefit is wasted on administrative timing.

Conclusion

Section 174A has since become a tool of survival in the 2026 startup ecosystem, having been turned into more of a cumbersome accounting footnote. The OBBBA can enable innovative firms to fund their growth through tax efficiency, bridging the gap between the requirement to pay payroll and the requirement to maintain an active R&D activity.

By

By

By

By